Investing isn’t just about picking the right mix of stocks

and bonds. It’s about understanding the forces that

influence markets and how your own behavior can impact

outcomes. Economic trends, government policy, and even

human psychology all shape the environment in which your

financial plan operates. By learning how these factors

interact, you can make more informed decisions and stay

focused on your long-term goals.

This blog builds on concepts from our Investing 201

webinar, which explored topics beyond the basics

introduced in Investing 101. If you missed the session,

you can watch the full webinar on our YouTube channel

here.

Understanding the Economy: The Big Picture

One way to think about the economy is like a balloon: it

can only expand so much, limited by factors like

population and productivity. There are only so many people

available to work, and each person can only produce so

much with the resources and technology at hand. When the

economy is growing, the balloon inflates as businesses

thrive, jobs increase, and confidence rises. Eventually,

it reaches its limit and sometimes stretches too far,

creating pressure that leads to a slowdown or even a

recession. When the economy slows, the balloon deflates as

spending pulls back and growth cools. When the economy

shifts, policymakers step in to guide it using monetary

and fiscal tools.

Who Helps Steer the Ship?

Governments and central banks use policy tools to guide

the economy, especially during challenging times. Back to

the balloon analogy: it is the job of policymakers to keep

the economy from stretching too far past its capacity and

to prevent contractions from being too severe.

•Monetary Policy: The Federal Reserve influences the

economy by setting interest rates and controlling the

money supply.

•Fiscal Policy: Government spending and tax policy also

play a role in driving growth or slowing it down.

For example, during the COVID pandemic, central banks

lowered rates while governments provided stimulus checks

to help households and businesses weather the storm. These

actions demonstrate how policy can cushion economic shocks

and support recovery.

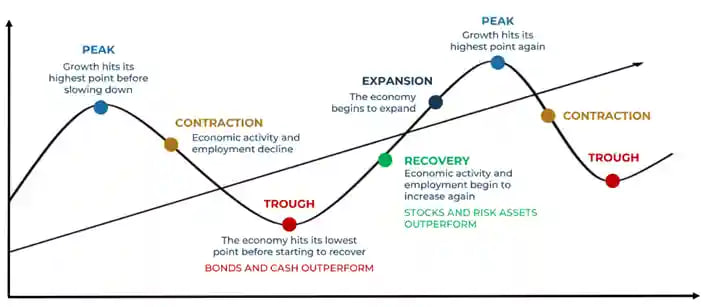

Market Cycles: The Ups and Downs Are Normal

Markets move through cycles of growth and contraction, and

understanding these phases can help you stay grounded when

volatility strikes. Different asset classes perform better

in different environments: stocks often thrive during

expansions, while bonds tend to shine during contractions.

Recognizing these patterns is key to maintaining

perspective and avoiding emotional decisions. The cycle

includes:

•Expansion: Businesses thrive, markets rise

•Peak: Growth slows, prices may begin to peak

•Contraction (Recession): Markets decline, but this phase

doesn’t last forever

•Recovery: Conditions improve and markets stabilize

History shows that market cycles are inevitable but

temporary. Over the past century, every recession has been

followed by recovery and growth. If that’s true, why not

sell when things look bad and buy back when things

improve? The challenge is that markets move ahead of the

economic cycle and often rebound before recovery is

confirmed. Every recession looks obvious in hindsight, but

in real time, even experts struggle to call the bottom or

the top. In fact, the National Bureau of Economic Research

(NBER), the official arbiter of U.S. recessions, makes its

announcements only after the fact. The committee waits for

revised data and clear evidence before declaring recession

start and end dates, which means those calls come well

after the market has already moved.

Behavioral Finance: Why Emotions Matter

Investing is as much about psychology as it is about

numbers. Emotions like fear and excitement can drive

investors to make poor decisions, such as buying high when

optimistic or selling low when fearful. Cognitive biases

like confirmation bias, mental accounting, and recency

bias can cloud judgment and lead to suboptimal

outcomes.

•Confirmation Bias: Seeking information that supports your

beliefs.

Example: You strongly believe tech stocks will outperform,

so you only read bullish articles and ignore reports

warning of risks.

•Mental Accounting: Treating money differently based on

its source.

Example: You receive a $2,000 tax refund and splurge on a

vacation because it feels like “extra” money, even though

it’s part of your ordinary income.

•Recency Bias: Assuming current trends will continue

indefinitely.

Example: After a year of strong stock gains, you assume

the rally will keep going and increase your equity

exposure aggressively, forgetting that markets move in

cycles.

Awareness of these behavioral biases is the first step

toward making better financial decisions. Emotions can

lead investors to react in ways that hurt long-term

results, such as selling when markets fall and buying only

after prices recover. Working with a financial advisor and

having a disciplined plan helps you stay on track and

avoid costly mistakes.

Bringing It All Together

Understanding these concepts helps you:

•Set realistic expectations: Markets will rise and fall,

and that’s completely normal. Staying focused on the long

term helps you avoid reacting to short-term noise.

•Diversify wisely: Don’t rely on one part of the market.

Different assets perform better in different phases of the

economic cycle, so a balanced mix can help reduce risk and

smooth returns.

•Partner with your advisor: Investing isn’t just about

numbers; it involves emotions too. A trusted advisor can

help you stay disciplined, recognize cognitive traps, and

keep your plan aligned with your goals and comfort

level.